The precarious state of the state: The economy

A sluggish pandemic recovery and high inflation squeezed UK living standards in the last parliament.

General election 2024

The next UK general election will be held on Thursday 4 July. Our analysis, explainers and events explore what happens before and during an election, how political parties and the civil service prepare for the outcome and what it means for government.

Find out more

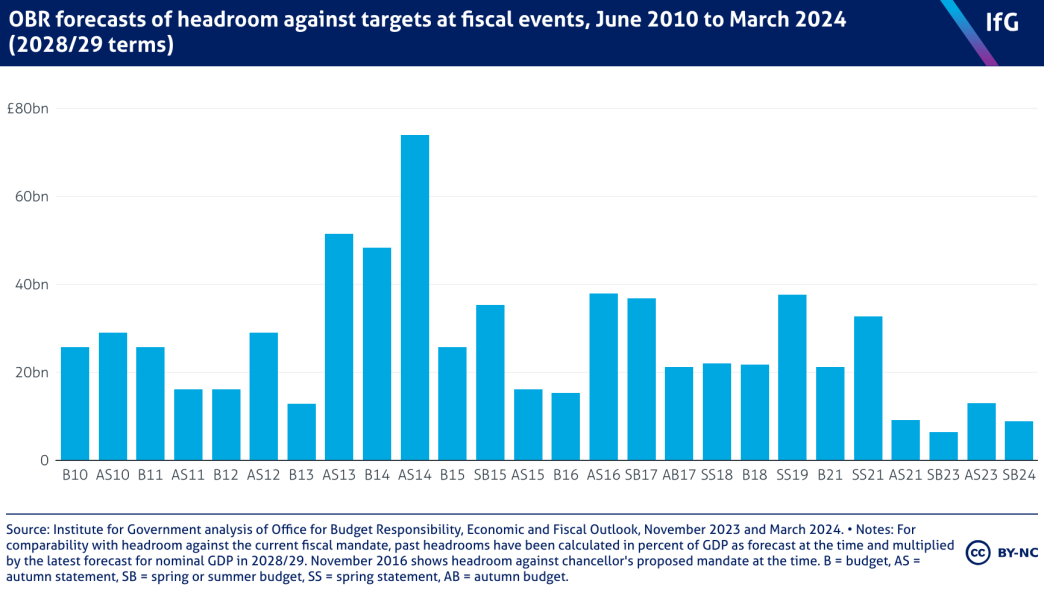

Fiscal rules are being met by the tightest of margins and on the basis of implausible spending assumptions

Both the Conservatives and Labour are committed to achieving the same target that debt should be on course to fall as a share of GDP between the fourth and fifth years of the latest forecast period. At the March budget, that meant debt had to be on course to fall between 2027/28 and 2028/29, though at the next forecast the horizon at which the rule must be met will roll forward an extra year.

This is a very loose fiscal rule compared to the debt targets that previous UK governments have tried to adhere to. However, given the current state of the UK’s public finances it still imposes severe constraints on how much more either party would be able to borrow. As the chart shows, the plans set out by the government in the March 2024 budget were only just consistent with that target: chancellor Jeremy Hunt had £8.9bn of headroom against this rule.

The amount of headroom that the government currently has against its target for debt to be falling in five years’ time is small – indeed Jeremy Hunt has averaged headroom at around a third of levels previous Conservative chancellors have maintained against their fiscal rules since 2010. This headroom is supposed to provide the chancellor with some flexibility to absorb economic and fiscal shocks without needing to change fiscal policy. Having such a small amount of headroom makes it more likely that a chancellor will be forced to adjust policy in response to relatively small forecast changes if he or she wants to remain on course to meet this target for debt.

And even this historically low level of headroom is only achieved through several questionable assumptions about the path of future policy that both parties have implicitly signed up to. Fuel duties have been frozen or cut in cash terms in every year since 2011, making the mooted 5p increase and subsequent uprating in line with inflation highly implausible. Income tax thresholds have already been frozen for the past two years, pushing more people into paying income tax or beginning to pay tax at the 40% marginal rate. A further four years of cash freezes will be difficult to maintain. But most significantly, public spending plans for the next few years imply further spending cuts in many areas, which will be very difficult to enact given the current state of, and predicted demand for, many of the UK’s public services.

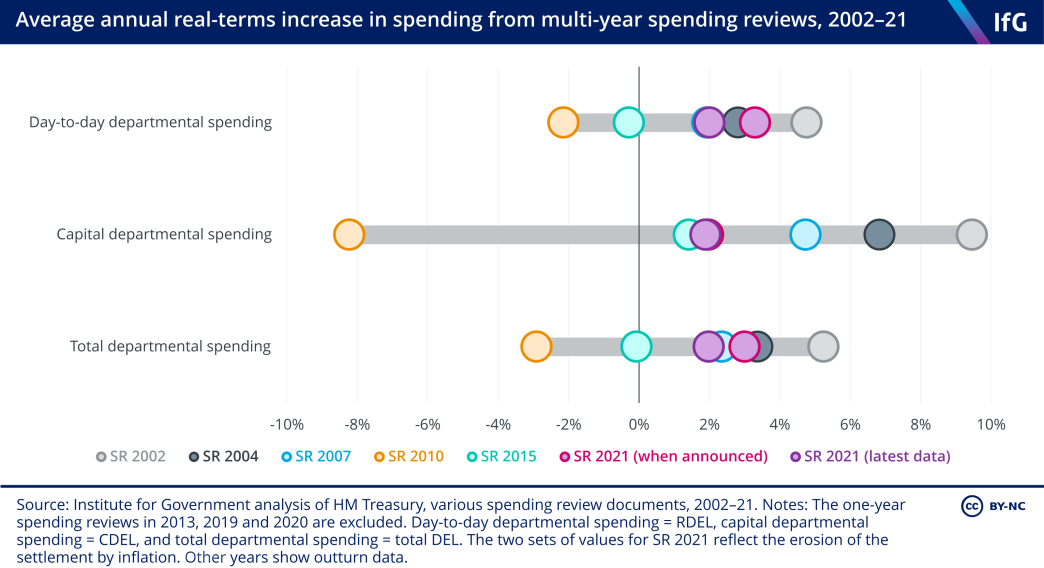

Spending plans set in 2021 have been eroded by unexpected inflation

At the time of the last multi-year spending review, in 2021, which set spending plans from 2022/23 to 2024/25, allocations appeared relatively generous. Day-to-day spending was expected to increase by 3.3% per year on average in real terms, similar increases to those planned in the 2002 and 2004 spending reviews, and a big change from the austerity of the 2010s. Capital spending plans were less generous, with increases of around 2% per year in real terms, similar to the 2015 spending review period.

Since departmental spending totals were set, however, inflation has been much higher than expected. While the government has topped up some budgets, it has not fully compensated departments’ day-to-day budgets for higher inflation, meaning average annual real-terms increases over the period are now expected to be 2.0% – that is, around a third lower than thought in 2021. While this is still higher than in the early 2010s and slightly above the 2017 parliament, it has not been sufficient to improve performance of most services, given the challenges facing public services that were exacerbated by the pandemic.

Current plans imply big real terms cuts to unprotected departments

For both day-to-day and investment spending, current plans imply tighter settlements for the next few years. Day-to-day spending is only set to increase by 1% per year in real terms. After accounting for commitments made to the NHS (through the 2023 workforce plan), education, defence, aid and childcare, this implies cuts of 2.6% per year in real terms for other services – which would come on top of cuts since 2010. 27 Chart D of Office for Budget Responsibility, Economic and Fiscal Outlook – March 2024, Cm 1027, The Stationery Office, 2024, retrieved 31 May 2024, www.obr.uk/efo/economic-and-fiscal-outlook-march-2024/.

The latest government plans are for public investment is to be broadly frozen in cash terms until 2028/29, leading to a sharp fall as a share of GDP – from 2.4% of GDP this year to 1.7% of GDP by 2028/29. Labour has made some extra commitments to invest towards its net zero target, but overall those plans still imply net investment falling sharply as a share of GDP. 28 Zaranko B, ‘A look under the hood of Labour’s investment plans’, blog, Institute for Fiscal Studies, 5 September 2023, retrieved 31 May 2024, ifs.org.uk/articles/look-under-hood-labours-investment-plans.

Firm spending plans from April 2025 are still to set, however the plans currently pencilled in will be difficult to deliver. Completing a spending review to set those plans, will be one of the first tasks facing the next government.

The timing of this will be important. The next government, whoever it is, will have to set spending plans for 2025/26 by the end of November 2024. There may be sufficient time for a spending review that sets multi-year budgets using existing processes and Whitehall architecture, however the timescale for doing this would be tighter than ever before. The alternative is to set one-year spending plans for 2025/26, creating more time to then run a full comprehensive and strategic multi-year spending review, concluding in the second half of 2025, that ensures spending is aligned with government priorities for the rest of the parliament.